Iran’s Oil Under Blockade Pressure: Will Caspian Routes and Storage Hold the Line?

April 16, 2026 — As the United States intensifies its maritime chokehold on Iran’s oil lifelines, Tehran faces a critical test of economic resilience. The blockade of the Strait of Hormuz — through which the vast majority of Iran oil exports flow — has effectively severed its primary revenue artery. With pre-blockade exports ranging between 1.5–1.84 million barrels per day (bpd), the sudden disruption threatens not just immediate income but the operational viability of Iran’s oil fields themselves.

The central question is no longer whether Iran can export oil — but whether it can avoid shutting down wells, an outcome that risks long-term reservoir damage and costly recovery.

The Blockade Shock — Why Southern Exports Have Collapsed

On April 13, 2026, following failed negotiations, US naval forces imposed a near-total maritime blockade targeting Iranian ports. Warships positioned across the Gulf of Oman and Arabian Sea have intercepted commercial shipping, forcing multiple vessels to turn back within the first 24 hours.

The impact is immediate and severe. Nearly 80–90% of Iran oil exports depend on southern maritime routes via the Strait of Hormuz. Pre-crisis exports exceeded 1.8 million bpd, but since the blockade began, there have been no confirmed successful tanker departures. The estimated economic loss stands at roughly $435 million per day, effectively translating into a near-complete shutdown of Iran’s primary export infrastructure.

Also Read: US Blockade of Iranian Ports Begins in Gulf of Oman and Arabian Sea

Economic Fallout — Revenue Collapse and the Risk of Well Shutdowns

Iran’s fiscal structure remains deeply dependent on hydrocarbons, with nearly 80% of government revenue tied to oil and gas exports. Even before the blockade, partial disruptions had already cost Tehran close to $5 billion in a single month.

The technical challenge now moves beyond revenue into field management. Storage facilities, including the critical hub at Kharg Island, provide only a limited buffer estimated at two to eight weeks. Once these capacities are exhausted, Iran will be forced to reduce or halt production. Such shut-ins are not routine operational adjustments; they carry the risk of permanent reservoir damage, especially in mature fields where pressure management is delicate. This elevates the crisis into a long-term strategic threat to Iran’s energy sector.

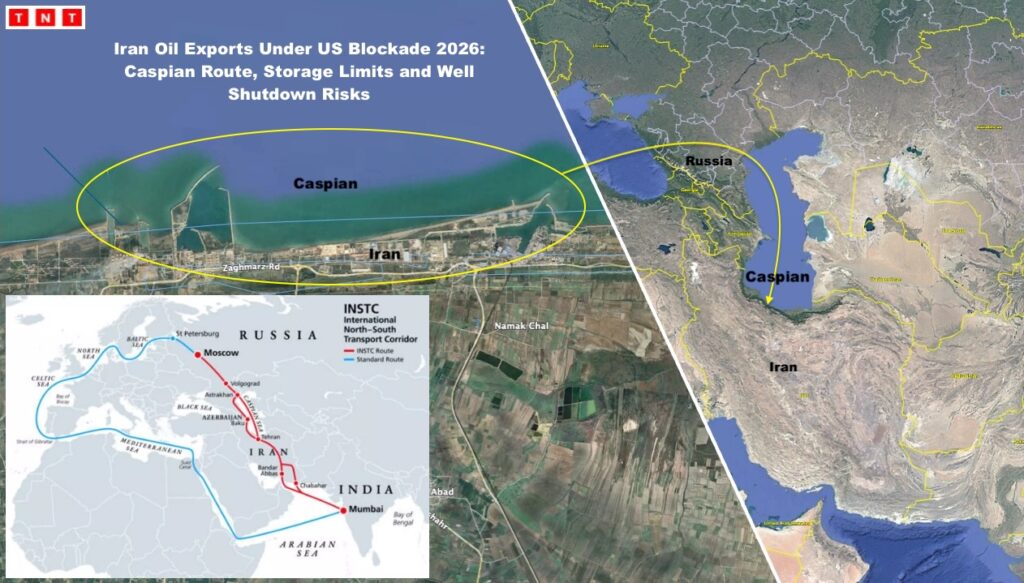

The Caspian Sea Corridor — Iran’s Northern Lifeline

Iran’s most viable alternative lies to the north through the Caspian Sea, integrated into the International North-South Transport Corridor (INSTC).

The system operates through northern ports such as Amirabad and Neka, from where oil and petroleum products are transported via smaller vessels across the Caspian to Russian ports like Astrakhan and Makhachkala. These flows are largely structured as swap arrangements, with Iran supplying crude or products and Russia compensating with equivalent volumes or refined fuels, which can then be redistributed through its pipeline network or onward into Eurasian markets.

However, the limitations are structural and significant. The Caspian’s vessel size restrictions — typically in the range of 3,000 to 6,000 tons — cap throughput at an estimated 50,000 to 100,000 bpd under current conditions. Moreover, the absence of a direct pipeline linking Iran’s major southern oil fields to its northern ports further constrains scalability.

Despite these limitations, the corridor carries considerable strategic value. It bypasses the Strait of Hormuz entirely, aligns with Russia’s logistical and geopolitical interests, and allows for multimodal flexibility combining maritime and rail transport. Yet, in absolute terms, it remains a partial mitigation tool rather than a replacement for southern exports.

Overland Routes — Limited and Inefficient Alternatives

Iran’s overland export options exist more in theory than in scalable reality. Rail and trucking routes connected through the INSTC can facilitate limited movement of refined products and small volumes of crude northward via Azerbaijan or Central Asia. However, these remain logistically constrained and economically inefficient for large-scale crude transport.

The Turkish corridor offers some connectivity, but its oil export infrastructure is limited and subject to political variability. Similarly, routes through Pakistan or deeper into Central Asia suffer from underdeveloped pipeline networks and long-standing project delays. Unlike regional competitors such as Saudi Arabia or the UAE, Iran has not developed major bypass pipelines that could redirect exports away from vulnerable maritime chokepoints.

As a result, overland routes provide only marginal relief, handling at best low tens of thousands of barrels per day, and cannot materially offset the blockade’s impact.

Storage — The Temporary Cushion

Iran’s storage infrastructure represents its most immediate buffer against the blockade. This includes a combination of onshore storage tanks, floating storage, and key terminal facilities, notably at Kharg Island, which remains largely intact.

Current estimates suggest that storage capacity can absorb excess production for approximately two to eight weeks under a full export halt. Historically, Iran has leveraged floating storage as a workaround during sanctions periods. However, under the present blockade, even tanker-based storage faces operational constraints due to restricted maritime movement.

Storage, therefore, functions as a delaying mechanism — buying time for diplomatic or logistical adjustments — but does not offer a sustainable long-term solution.

Strategic Reality — Can Iran Sustain Its Oil System?

When assessed collectively, Iran’s alternatives form a layered but inadequate response framework. The Caspian Sea route emerges as the most effective immediate option, capable of sustaining between 50,000 and 100,000 barrels per day and operational within days to weeks. It carries high strategic value due to Russian partnership and integration with the INSTC, yet remains fundamentally limited by vessel size and infrastructure gaps.

Overland routes through neighboring countries contribute additional volumes, but only in the range of low tens of thousands of barrels per day, and are constrained by both infrastructure and geopolitical risks. Their role is supplementary rather than transformative.

Storage provides the most immediate relief, offering a buffer window of up to two months, but it is inherently finite. Once capacity is reached, production cuts become unavoidable, bringing with them the risk of well damage.

In contrast, Iran’s southern export system — capable of handling over 1.5 million bpd under normal conditions — remains entirely non-operational under US naval enforcement.

Strategic Conclusion — Holding Pattern, Not a Solution

Iran’s current strategy is one of managed survival: maximize northern exports, utilize storage capacity, and attempt to outlast the blockade. However, the imbalance between pre-crisis export capacity and current alternatives is stark.

At best, Iran can sustain less than 10% of its previous export volumes through these combined measures. Storage delays the crisis but does not eliminate it, and prolonged disruption raises the probability of irreversible production losses.

The broader geopolitical implications are equally significant. Russia stands to gain from enhanced Caspian integration, while China may continue accessing discounted Iranian oil through indirect channels. Meanwhile, global oil markets are tightening, with prices approaching $100 per barrel, reflecting the systemic impact of the disruption.

The crisis has elevated the Caspian Sea into a strategically important, though inherently constrained, energy corridor. For Iran, it offers a lifeline — but not an escape.