Black Ghosts on the Water – Russian Oil Tankers and the New Asian Uncertainty

The sea was never truly quiet that February.

It rolled beneath a low ceiling of grey cloud, pressing down on every horizon. Salt air carried the metallic smell of diesel and crude. In this unsettled water, Russian oil tankers drifted without clear destination, carrying cargoes that suddenly had fewer buyers.

Captain Elena Markov stood on the starboard wing of the Northern Star, an Aframax tanker nearing three decades of service. Rust streaked its hull. Paint peeled in long strips. She pulled her jacket tight against the cold wind and watched the slow movement of waves below.

Beneath her feet lay 120,000 barrels of Russian Urals crude. For years, this oil had flowed steadily to Indian refineries. Jamnagar, Paradip, Mumbai, and Kochi had become familiar destinations. Discounted Russian crude had powered India’s refining boom after 2022.

However, that rhythm had broken.

A Sudden Shift in Energy Routes

Three days earlier, trading desks and shipping firms received troubling signals. A new understanding between Washington and New Delhi had begun reshaping oil flows. Lower tariffs on Indian exports to the United States reportedly came with an unwritten condition. India was expected to reduce or halt Russian oil purchases.

President Trump publicly linked trade relief with energy realignment. Meanwhile, the Modi government offered no detailed clarification. This silence unsettled markets. As a result, refiners delayed tenders. Discharge schedules disappeared. Charterers stopped issuing clear instructions.

The last message Elena received was simple: Await further orders.

Her vessel was now marked “For Orders” on AIS screens. So were many others.

A Floating Inventory Without Buyers

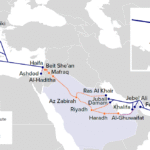

Across East Asian waters, more than a dozen Russian oil tankers waited. Some lingered near Malaysia. Others hovered close to the Singapore Strait. A few moved near disputed islands in the South China Sea. Several stayed near Russia’s Pacific approaches.

Together, they carried between 10 and 12 million barrels of Urals crude.

Some vessels signalled “China for orders.” Others positioned themselves for possible ship-to-ship transfers. A few simply circled slowly to save fuel.

In January 2026, India still imported around 1.2 million barrels per day of Urals crude. This was already below the 2024 peak of more than two million barrels. Yet it provided stability. When that demand weakened, surplus volumes flooded the market.

Chinese independent “teapot” refiners increased purchases to about 500,000 barrels per day. This was a monthly record. However, it remained insufficient.

Moreover, these refiners preferred lighter grades like ESPO and Sokol. Urals crude is heavier and more sulphur-rich. Therefore, processing costs are higher. Indonesia and other regional buyers also favoured lighter blends.

As a result, buyers hesitated.

Markets React to Growing Oversupply

Within days, price discounts widened. The gap between Urals and Brent expanded again. Traders in Singapore, Dubai, Geneva, and Shanghai recalculated margins and storage costs. Floating storage became expensive. Freight rates climbed.

Sellers faced pressure. Buyers gained leverage.

Elena remembered earlier years, before sanctions and rerouting. Urals once traded close to Brent. The market had seemed predictable. Since 2022, equilibrium had repeatedly shifted. Each shock produced a new balance. Yet this time felt different.

This was political.

Decisions taken in Washington and New Delhi now shaped routes thousands of miles away. Crews and ships felt their impact first.

Somewhere in Beijing, traders prepared low offers. In Moscow, revenue forecasts were revised. In New Delhi, refinery managers waited for policy signals.

At sea, uncertainty prevailed.

Black Ghosts on a Silver Sea

The Northern Star turned gently into the current. Its bow pointed east-southeast. There was no confirmed destination. There was only movement.

Around her, other Russian oil tankers did the same.

They moved slowly. They conserved fuel. They waited.

On satellite images, they appeared as dark shapes on pale water. To traders, they represented risk. To policymakers, they were bargaining tools. To crews, they were homes suspended in uncertainty.

Black ghosts on a silver sea, carrying oil no one had yet agreed to buy.

The Real Story Behind the Imagery

According to Bloomberg, dated February 6, 2026, more than a dozen tankers loaded with Russian Urals crude are currently en route to or idling in East Asian waters after Indian refiners sharply reduced purchases.

Key Reported Facts

Indian imports of Urals fell to about 1.2 million barrels per day in January 2026, down from more than 2 million bpd in 2024.

The reduction is linked to a new US–India trade framework under President Trump, connecting tariff relief with energy realignment.

China’s teapot refiners lifted a record 500,000 bpd of Urals in January, yet this failed to absorb surplus supply.

Additional tankers from the Baltic, Mediterranean, and Red Sea are now signalling East Asia as their destination.

Discounts on Urals crude have widened as sellers face oversupply risks.

Whether this shift proves temporary or structural remains uncertain. However, one reality is clear. The geopolitics of energy continues to reshape global trade, barrel by barrel, across open water.