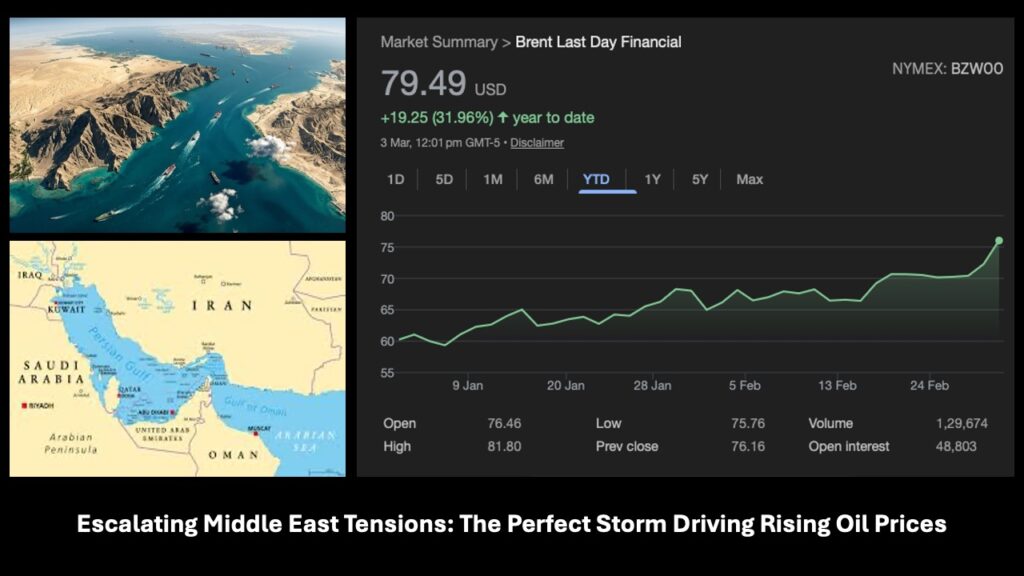

Escalating Middle East Tensions: The Perfect Storm Driving Rising Oil Prices and Its Impact on India

Global energy markets have entered a phase of extreme volatility following the escalation of conflict in the Middle East after US – Israeli strikes on Iran on February 28, 2026. Assassination of Iran’s Supreme Leader Ayatollah Ali Khamenei and subsequent retaliatory attacks have intensified fears of a prolonged regional war. As a result, rising oil prices have emerged as the most immediate economic consequence of the crisis.

Brent crude futures surged by nearly 13.6 per cent in a single day, crossing $83 per barrel on March 3, 2026, a twelve-month high. Meanwhile, West Texas Intermediate followed a similar trajectory. What began as targeted military action has now expanded into a broader disruption of energy infrastructure and shipping routes. Consequently, analysts warn that prices could move towards $100 per barrel if tensions persist, echoing the oil shocks of the 1970s.

This report examines the key drivers behind the surge in crude prices and analyses how the crisis could reshape India’s economic outlook.

The Cascade of Disruptions Behind Rising Oil Prices

Iranian Oil Exports and Production Shutdown

Iran, OPEC’s fourth-largest producer with output of around 3.3 million barrels per day, has witnessed a sharp decline in exports since the outbreak of hostilities. Damage to critical facilities and sustained military pressure have disrupted production and logistics. In addition, Tehran’s threats to restrict oil flows have further isolated its exports.

As a result, nearly three per cent of global oil supply has effectively disappeared from the market. This sudden loss has created immediate tightness and intensified speculative activity.

Strait of Hormuz Under Siege

The Strait of Hormuz, which handles nearly 20 per cent of global oil and significant volumes of liquefied natural gas, has become a focal point of risk. Iran has warned commercial vessels against transit, while major insurers have withdrawn war-risk coverage.

More than 150 tankers remain anchored outside the strait. Consequently, shipments of up to 20 million barrels per day from Saudi Arabia, Iraq, and the UAE have been disrupted. Even without a formal blockade, the perceived risk has driven freight and insurance costs sharply higher.

Saudi Aramco and Gulf Production Disruptions

Saudi Aramco temporarily shut down its 550,000 barrels-per-day Ras Tanura refinery after an Iranian drone attack on March 2, 2026. Although damage was limited, authorities halted operations as a precaution.

In addition, several Gulf producers initiated partial shutdowns to safeguard infrastructure. Facilities in Qatar and Iraqi Kurdistan also reduced output. These measures have further constrained supply and pushed diesel and gasoil futures up by nearly 20 per cent.

Saudi Arabia has redirected some exports through Yanbu on the Red Sea. However, this alternative route has limited capacity and cannot fully offset losses from the Gulf.

Red Sea Shipping Crisis and Houthi Attacks

The conflict has also spilled into the Red Sea. Iran-backed Houthi militants in Yemen have resumed attacks on commercial vessels near the Bab-el-Mandeb Strait.

Major shipping firms, including Maersk and Hapag-Lloyd, have suspended transits through the region. Consequently, vessels are now rerouting around the Cape of Good Hope. This detour adds several weeks to delivery times and increases costs by billions of dollars.

Moreover, container freight rates have surged by $1,500 to $3,500 per unit, worsening global supply delays.

Global Supply Pressures and Market Reactions

Venezuela’s Limited Capacity to Compensate

With Middle Eastern supplies under threat, attention has shifted to Venezuela, which holds the world’s largest proven reserves of around 303 billion barrels. However, years of mismanagement, sanctions, and underinvestment have weakened its oil sector.

Current production stands near one million barrels per day. Experts estimate that restoring meaningful capacity would require investments of $80–100 billion and up to ten years. In addition, much of Venezuela’s output consists of heavy and extra-heavy crude, which requires specialised refining facilities. At present, only a limited number of refineries, mainly in India and China, can process this grade efficiently.

Logistics further constrain Venezuelan exports. Most shipments to Asia must pass through the Red Sea, exposing vessels to Houthi attacks and rising insurance costs. Alternatively, tankers can route around the Cape of Good Hope. However, this route is significantly longer, faces rough weather conditions, and increases transit time and fuel expenses. As a result, it remains a commercially unattractive option.

Therefore, despite its vast reserves, Venezuela cannot provide meaningful short-term relief to global markets during the current crisis.

Risk of a Protracted Conflict

Iranian officials, including Supreme National Security Council Secretary Ali Larijani, have stated that the country is prepared for a long war. At the same time, US leaders have acknowledged that operations could extend beyond initial projections.

Meanwhile, regional proxies, including Hezbollah, continue to engage in hostilities. As a result, markets have priced in a sustained “war premium”. Reported casualties in Iran have approached 800, while US forces have also suffered losses.

Without a clear diplomatic roadmap, uncertainty remains elevated.

Hoarding by Major Importers

Major consuming nations have begun stockpiling crude to protect against shortages. China has reportedly accumulated reserves of nearly 1.4 billion barrels and may add another 170 million barrels in 2026.

The United States continues to manage its Strategic Petroleum Reserve. In addition, private refiners have increased inventory levels. This behaviour removes supply from circulation and amplifies price pressures.

Impact of Rising Oil Prices on India’s Economy

India imports nearly 85 per cent of its crude oil requirements, with about half passing through the Strait of Hormuz. Therefore, the country remains highly exposed to Middle Eastern instability.

Economists estimate that a sustained $10-per-barrel increase could widen India’s current account deficit by 0.5 per cent of GDP. It could also raise consumer inflation by 0.3 to 0.4 percentage points and reduce growth by up to 0.3 per cent.

Fuel Prices and Household Burden

Petrol and diesel prices could rise by 10 to 20 per cent if elevated crude levels persist. Although oil marketing companies may initially absorb losses, prolonged pressure will likely lead to retail adjustments.

Consequently, household transport and commuting costs could rise significantly.

Inflation and Food Costs

Transportation accounts for nearly 25 to 45 per cent of India’s consumer price basket through food and goods movement. Higher diesel prices increase freight charges and raise prices of vegetables, grains, and packaged foods.

Therefore, food inflation may accelerate in coming months.

Aviation, Logistics, and Trade

Red Sea disruptions and longer shipping routes have increased logistics expenses. Airlines face higher jet fuel costs, while exporters encounter rising freight bills.

As a result, airfares and shipping charges may rise further, affecting trade competitiveness.

Currency and Borrowing Pressures

Rising oil prices typically weaken the rupee by increasing import bills. With the currency already trading beyond 91 per dollar, further depreciation could intensify inflation.

Moreover, elevated price levels may delay interest rate cuts by the Reserve Bank of India. This would keep home and auto loan rates high and restrict consumer spending.

Broader Economic Effects

India receives annual remittances of $40–50 billion from Gulf workers. A prolonged conflict could reduce employment opportunities in the region and affect inflows, particularly to Kerala and Uttar Pradesh.

Industries such as paints, FMCG, and automobiles also face higher input costs. Meanwhile, stock markets fell sharply on March 2, reflecting weakened investor confidence.

Mitigation measures include diversifying imports towards the US and Latin America, using strategic reserves, and extending selective subsidies. However, with FY26 oil imports already nearing ₹8.8 lakh crore, fiscal pressures remain significant.

Outlook for Global Energy Markets

OPEC+ and non-OPEC producers, including the United States, possess some spare capacity. However, rapid scaling remains uncertain amid security risks.

Some forecasts suggest that prices could return to $50–60 per barrel by mid-2026 if tensions ease. Nevertheless, continued hostilities could sustain elevated levels for much longer.

With diplomacy struggling to gain traction, energy markets remain on edge. For India, the coming months may determine whether rising oil prices translate into a prolonged phase of economic strain or a temporary disruption.