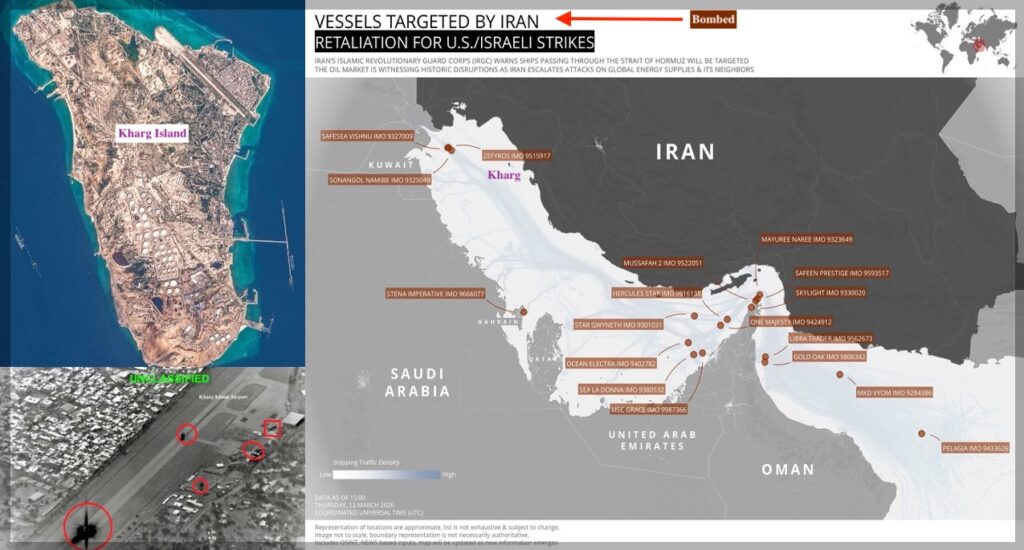

Kharg Oil Disruption and Hormuz Closure Send Shockwaves Across Asian Economies

Tattvam News Today | March 14, 2026 | Delhi

A United States strike on Iran’s main oil export terminal at Kharg Island combined with threats by Iran to close the Strait of Hormuz (Kharg-Hormuz Oil disruption) has created one of the most serious energy security scenarios the global oil market has faced in decades.

The Persian Gulf chokepoint is the most critical artery in the world’s petroleum trade. Roughly 17–20 million barrels of oil per day pass through the Strait of Hormuz, accounting for about 20% of global oil consumption and nearly one-third of seaborne crude trade.

If Iran’s export hub at Kharg Island is disabled while tanker traffic through Hormuz is disrupted, the global energy system would face a dual shock: Iranian exports collapse at the source while shipments from other Gulf producers struggle to reach international markets.

Because Asian economies depend heavily on Persian Gulf energy supplies, the consequences would fall most heavily across the region.

The Strategic Importance of Kharg Island in Iran’s Oil Exports

The island terminal of Kharg serves as the backbone of Iran’s oil export infrastructure.

Located about 25 kilometres off Iran’s southwestern coast in the Persian Gulf, the facility handles around 90 – 95% of Iran’s crude exports, which in recent months have been estimated between 1.5 and 1.7 million barrels per day despite international sanctions.

Tankers departing Kharg Island supply refiners primarily in Asia, with the majority of shipments heading toward Chinathrough intermediary trading channels.

Disruption at Kharg therefore immediately removes a significant volume of crude from global markets.

If exports from the terminal halt while the Strait of Hormuz becomes unsafe for tanker navigation, the result would be a compounded supply shock affecting not only Iranian crude but also oil shipments from neighbouring Gulf producers.

Strait of Hormuz: The World’s Most Critical Oil Chokepoint

The Strait of Hormuz links the Persian Gulf to the Arabian Sea and the wider Indian Ocean.

According to global shipping data, the waterway carries oil exports from several major producers, including:

- Saudi Arabia (partial on Persian Gulf side)

- United Arab Emirates (partial on Persian Gulf side)

- Iraq (complete)

- Kuwait (complete)

- Qatar (complete)

- Bahrain (complete)

Together these countries export roughly 20 million barrels per day through the strait, a volume equivalent to nearly one-fifth of the world’s daily oil consumption, which currently stands near 102 million barrels per day.

Energy markets are highly sensitive to disruptions in the region. Even the threat of conflict has historically pushed prices sharply higher. During earlier crises in the Gulf, Brent crude prices have risen 10–20 % within days as traders price in the risk of supply interruptions.

A prolonged disruption would also drive up marine insurance premiums for tankers, which surged more than 400 % during earlier Gulf tensions, adding further cost pressure to global oil shipments.

China Faces the Largest Immediate Supply Shock

Among major economies, China would experience the largest immediate supply disruption.

Over the past several years China has become the dominant buyer of Iranian crude, purchasing between 1.3 and 1.6 million barrels per day, most of it destined for independent refineries known as “teapot” refiners.

These facilities rely heavily on discounted Iranian crude, which often trades $8–12 per barrel below benchmark prices.

A disruption at Kharg Island would abruptly halt those flows. At the same time, instability in the Strait of Hormuz could complicate shipments from other Gulf producers.

China maintains one of the world’s largest strategic petroleum reserves, estimated to cover three to four months of imports, but replacing large volumes of discounted crude with higher-priced international supplies would still impose significant economic costs.

Japan and South Korea Vulnerable to Hormuz Shipping Disruptions

The economies of Japan and South Korea are particularly vulnerable to disruptions in the Strait of Hormuz because of their long-standing reliance on Middle Eastern oil.

Both countries obtain roughly 70–90 % of their crude imports from the Persian Gulf, with most shipments passing through Hormuz.

Japan consumes around 3.4 million barrels of oil per day, while South Korea consumes roughly 2.7 million barrels per day, making uninterrupted tanker flows essential for their industrial economies.

However, both nations have prepared extensively for such crises.

Japan maintains strategic petroleum reserves covering approximately 230 days of consumption, while South Korea holds between 110 and 200 days depending on demand levels. These stockpiles provide a substantial buffer against short-term disruptions.

India Faces Long-Term Economic Pressure

For India, the crisis presents a different set of risks.

India imports about 80–85 % of its crude oil needs, and roughly half of those imports originate in the Persian Gulf. Key suppliers include Saudi Arabia, Iraq, Kuwait and the United Arab Emirates.

Although India currently imports little Iranian oil, a closure of the Strait of Hormuz would disrupt the primary shipping route for much of its energy supply.

India’s strategic petroleum reserves currently cover roughly 70 – 80 days of consumption, significantly less than the reserves held by Japan or China.

A sustained spike in oil prices would therefore have broader economic consequences, including:

- Higher fuel inflation

- Pressure on government subsidies

- A widening trade deficit

- Currency volatility

Because India is among the world’s fastest-growing energy consumers, prolonged high oil prices could also slow economic expansion.

Europe Relatively Shielded from Direct Disruption

In contrast to Asia, Europe’s direct exposure to Persian Gulf disruptions is relatively limited.

European countries import almost no Iranian crude and obtain only a small share of their oil through shipments passing the Strait of Hormuz.

Supplies from the United States, Norway, West Africa and the North Sea have diversified Europe’s energy mix in recent years.

While global price spikes would inevitably affect European consumers, the region would likely experience less immediate supply disruption than Asian economies.

Russian Oil Provides Partial Buffer for Asia

One important shift in recent years has been the growing role of Russian crude in Asian energy markets.

Since the Ukraine war reshaped global oil trade flows, Russia has redirected significant volumes of oil toward Asia.

Russian supplies now account for:

- 17–20 % of China’s oil imports

- Up to 30 % of India’s imports during certain periods

These additional supplies provide some diversification away from the Persian Gulf.

However, Russian exports cannot fully replace the massive volumes of oil that transit the Strait of Hormuz each day.

A Crisis with Global Economic Consequences

The combination of a strike on Kharg Island and a disruption of tanker traffic through the Strait of Hormuz would represent one of the most severe supply shocks to global oil markets since the early 1990s Gulf War.

Energy markets would immediately face the loss of Iranian exports alongside the risk of disrupted shipments from several of the world’s largest oil producers.

Because Asia absorbs nearly 85 % of all crude shipments passing through the Strait of Hormuz, the economic impact would fall most heavily on the region’s largest importers.

For the global economy, the crisis would serve as a stark reminder that a single island terminal and a narrow maritime passage in the Persian Gulf still hold extraordinary power over the world’s energy security.

ALSO READ:

Hormuz Crisis Pushes Oil Towards $200: Global Economic Shock Looms

Kharg Island: America’s Calculated Strike and Iran’s Looming Economic Checkmate

Amid Hormuz Oil Shock, India’s Refiners Find Opportunity As India Increases Russian Crude Import